In a world flooded with budgeting apps, money hacks, and financial gurus, most people still struggle to save. A recent 2024 survey found that over half of Americans don’t have enough savings to handle a $1,000 emergency expense. I used to be one of them—until I tried one trick that changed everything.

In just 12 months, using this strategy, I saved $10,000 without increasing my income. No side gigs. No sacrificing essentials. Just one behavioral shift.

The Secret? The Reverse Budget (also called “Pay Yourself First”)

What Is It?

Most people budget like this:

Income comes in, expenses go out, and whatever remains—if anything—is set aside for savings.

But the Reverse Budget flips that model:

Earn → Save First → Spend What’s Left

It’s not new. In fact, it’s a strategy rooted in behavioral finance and popularized by experts like George Clason (The Richest Man in Babylon) and later modernized by financial planners.

“Don’t save what is left after spending; spend what is left after saving.” — Warren Buffett

Why It Works: Behavioral Psychology + Automation

Studies in behavioral economics show that we struggle with deferred gratification—saving for later—because we view money as more valuable now than in the future.

So how do we outsmart ourselves? By removing the choice.

Behavioral studies at Harvard and MIT confirm that automated savings increase long-term wealth because they bypass willpower.

Fintech apps using this model report 2x–4x higher savings rates among users.

How I Saved $10,000 in 12 Months: Step-by-Step

- I Calculated My Target

I set a clear objective to build up $10,000 in savings within 12 months.

Breakdown:

$10,000 ÷ 12 months = ~$834/month

I used a simple reverse budgeting calculator to visualize it.

Download my free spreadsheet: Budget Calculator Spreadsheet

- I Automated It

Using my online bank, I set up:

A recurring monthly transfer of $850 on payday

Sent to a separate high-yield savings account (2.75% APY in 2024)

This made saving effortless—and invisible.

- I Adjusted My Spending After Saving

When you “hide” your savings before you see it, your brain starts treating your remaining income as your real budget. And it works.

I cut unnecessary subscriptions, cooked more at home, and avoided impulse spending. But I didn’t feel deprived—I felt in control.

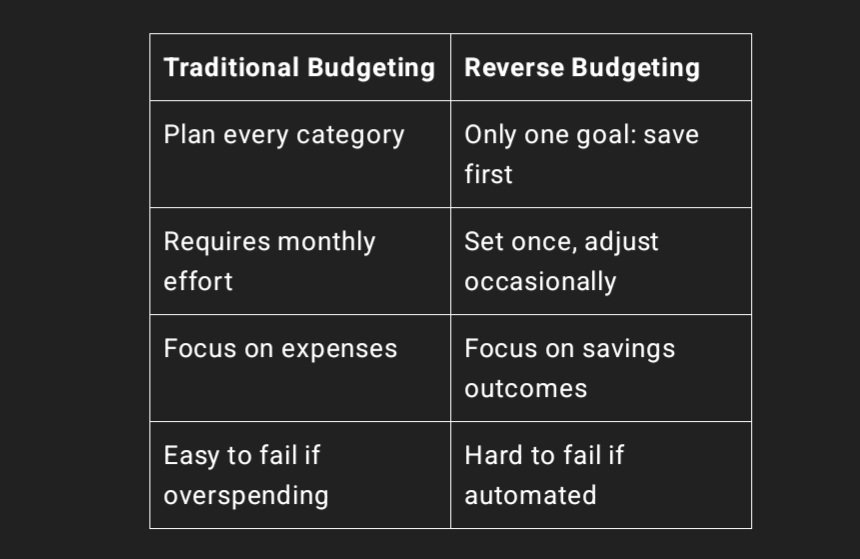

Traditional Budget vs. Reverse Budget

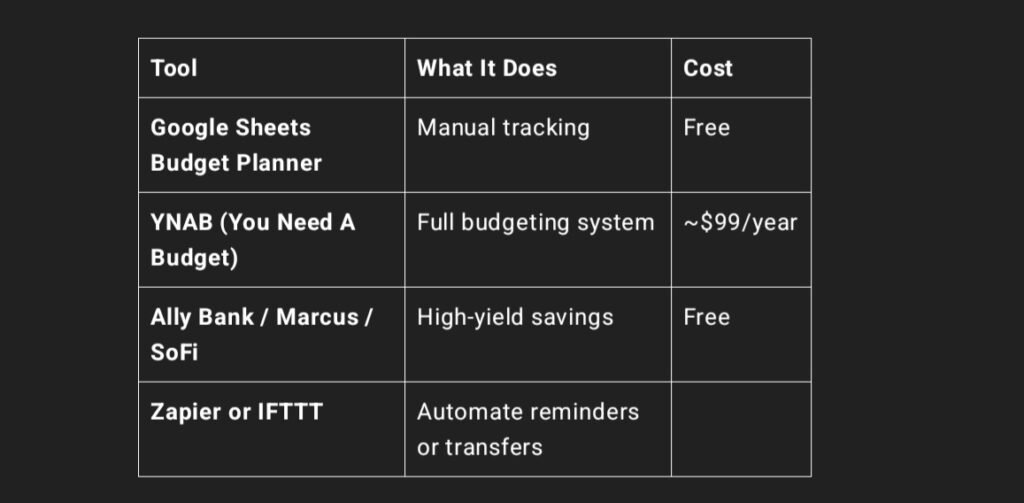

Tools That Helped Me Succeed

Results I Experienced

Reaching the $10,000 mark was the biggest annual savings milestone I had ever achieved.

Emergency fund built — better peace of mind

Avoided lifestyle creep — didn’t inflate spending with income

Improved financial confidence — guilt-free spending after saving

Who This Works Best For

This strategy works well for:

People with a stable monthly income

Those who hate micromanaging budgets

Anyone trying to build an emergency fund or save for a big goal

It may not be ideal if:

You have highly irregular income

You need to pay off high-interest debt first

3-Minute Action Plan

- Break down your yearly savings goal into manageable monthly amounts

- Open a separate savings account

- Set an auto-transfer on payday

- Track your remaining budget weekly

Final Takeaway

The reason most budgets fail isn’t complexity—it’s friction.

The reverse budgeting method removes friction. It’s not flashy, but it works.

In 2025, when inflation and rising living costs threaten every paycheck, building savings has to be automatic—not optional.

If I could save $10,000 on an average income, you can too—with a simple plan, consistency, and one small shift.

Follow Us On WhatsApp

Follow Us On WhatsApp

Leave a Comment